SC Declares Coconut Oil an Edible Product: Resolving a Tax Debate Spanning Over a Decade

- M.R Mishra

- Dec 21, 2024

- 3 min read

The classification of coconut oil under India’s tax regime has been a subject of extensive legal and regulatory debate for more than 15 years.

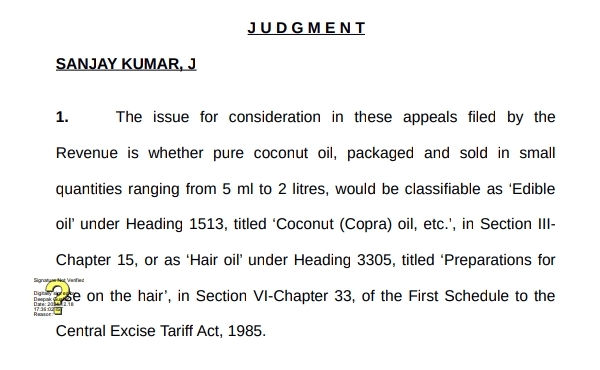

CIVIL APPEAL NO. 1766 OF 2009

Commissioner of Central Excise, Salem …Appellant

Versus

M/s. Madhan Agro Industries (India) Private Ltd. …Respondent

WITH

CIVIL APPEAL NOS. 6703-6710 OF 2009

Supreme Court resolved a 15-year tax dispute on coconut oil classification.

- Coconut oil in 5 ml to 2-liter packs classified as edible oil unless explicitly labeled as hair oil.

- Edible oil taxed at 5% under GST, while hair oil is taxed at 18%.

- Small packaging size alone is not a determinant for classification as hair oil.

- Labels and marketing must indicate cosmetic use for classification as hair oil.

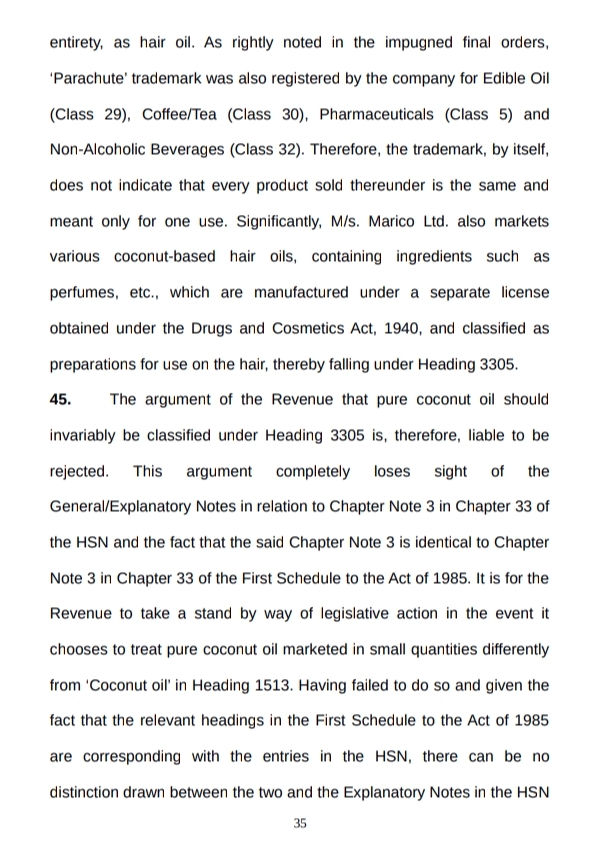

- Advertisements or trademark registration do not conclusively determine classification.

- Agmark certification supported classification of "Shanti Coconut Oil" as edible.

- Ruling aligns with 2005 Harmonized System of Nomenclature (HSN) amendment.

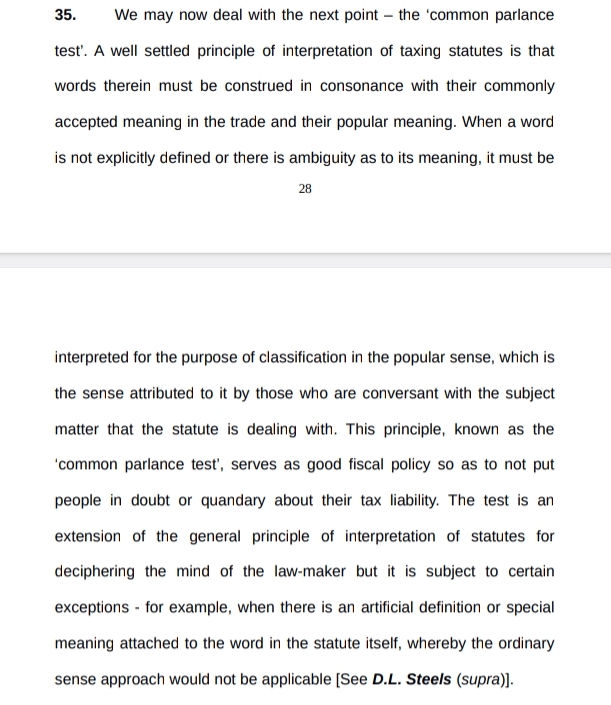

- Rejects reliance on the "common parlance test" for classification disputes.

The Judgement:

The core question was whether coconut oil should be taxed as an edible oil or as a haircare product. Under the Goods and Services Tax (GST) framework, introduced in 2017, edible oils are taxed at a concessional rate of 5%, while haircare products attract a significantly higher rate of 18%.

The Supreme Court, in a definitive judgment on December 18, 2024, settled this longstanding dispute by ruling that coconut oil should be classified as an edible oil, irrespective of packaging size, thereby attracting the lower tax rate.

Before the introduction of GST, coconut oil’s tax treatment was governed by the Central Excise Tariff Act, 1985. The 2005 amendment to the Act placed coconut oil under the category “Animal or Vegetable Fats and Oils and their Cleavage Products; Prepared Edible Fats; Animal or Vegetable Waxes,” with an excise duty of 8%.

This classification differentiated it from haircare products, which were taxed at a higher rate of 16% under the category

“Preparations for use on the hair.”

However, ambiguity arose when the Central Board of Excise and Customs (CBEC) issued a circular in 2009, classifying coconut oil sold in small containers (less than 200 ml) as hair oil, thereby subjecting it to the higher tax rate. Following legal challenges, this circular was eventually withdrawn in 2015.

The dispute intensified when several manufacturers, including Madhan Agro Industries, challenged show-cause notices from excise authorities that sought to classify coconut oil in small packages as a haircare product. The Customs, Excise and Service Tax Appellate Tribunal (CESTAT) consistently ruled in favor of the manufacturers, asserting that coconut oil is primarily an edible oil, regardless of packaging size or intended use. These rulings were subsequently appealed by the Commissioner of Central Excise in the Supreme Court.

In 2018, the Supreme Court delivered a split verdict on the issue. Justice Ranjan Gogoi held that coconut oil, irrespective of the size of its container, should be classified as an edible oil. On the other hand, Justice R Banumathi applied the "common parlance test," arguing that coconut oil sold in small containers is generally perceived by consumers as hair oil and should therefore be taxed as such.

This split decision left the matter unresolved.

The case culminated in 2024, with a bench comprising Chief Justice of India Sanjiv Khanna and Justices Sanjay Kumar and R Mahadevan delivering a final verdict.

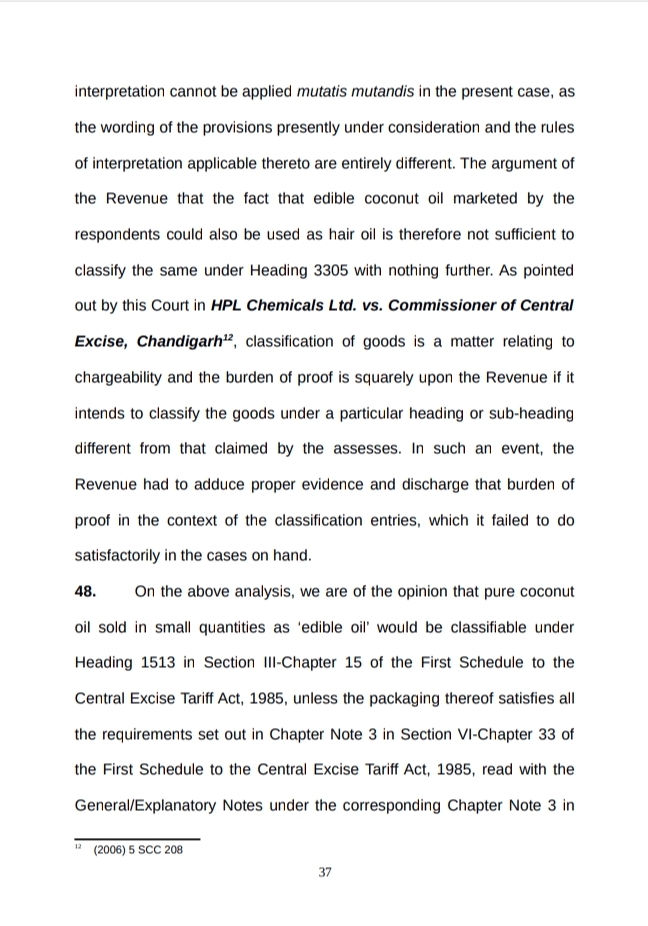

The court ruled that legal classifications under the Harmonized System of Nomenclature (HSN) take precedence over market perceptions. It rejected the application of the "common parlance test" in this case, stating that it is applicable only when a product lacks a clear legal definition.

The judgment emphasized that the multifunctional nature of coconut oil—capable of being used as both an edible oil and a cosmetic—does not warrant its exclusion from the edible oil category.

The court also clarified that container size is not a definitive criterion for distinguishing edible oils from haircare products, noting that small-sized containers are commonly used for both categories.

Furthermore, it referred to the Standards of Weights and Measures (Packaged Commodities) Rules, 1977, which specify permissible packaging sizes for edible oils, including small containers.

This landmark ruling not only settled the tax ambiguity surrounding coconut oil but also underscored the importance of adhering to precise legal classifications under India’s tax regime.

The decision is expected to provide clarity to manufacturers, consumers, and tax authorities, ensuring uniformity in the treatment of coconut oil across the country.

Supreme Court Verdict

CIVIL APPEAL NO. 1766 OF 2009

Commissioner of Central Excise, Salem …Appellant

Versus

M/s. Madhan Agro Industries (India) Private Ltd. …Respondent

WITH

CIVIL APPEAL NOS. 6703-6710 OF 2009

Thanks For Visiting!!

Comments